Executive summary

- Investors require adequate income whilst protecting and growing capital

- Today’s investment challenges

- A framework to review retirement income products

- A solution: buy blue chip high yielding shares for income, with insurance

The Federal Government is committed to facilitate better retirement income products.

“We want to facilitate better retirement products that allow retirees to improve their standards of living”, Assistant Treasurer Kelly O’Dwyer stated recently when addressing the Committee for Economic Development of Australia.

“… the retirement phase of superannuation is underdeveloped and provides limited choice for managing risk”

David Murray, Chair of The Financial System Inquiry

The Financial System Inquiry listed 3 criteria for “comprehensive retirement income products.”

- Regular and stable income

- Longevity: invest in growth assets

- Flexibility: low cost, ‘cooling off’ period

The Lonsec report referred to above considers the asset classes commonly used to generate retirement income:

· Term deposits

· Annuities

· Endowment Bonds

· Bond funds

· Equities – income focused

· Hybrids

Most “income” alternatives don’t invest in growth assets.

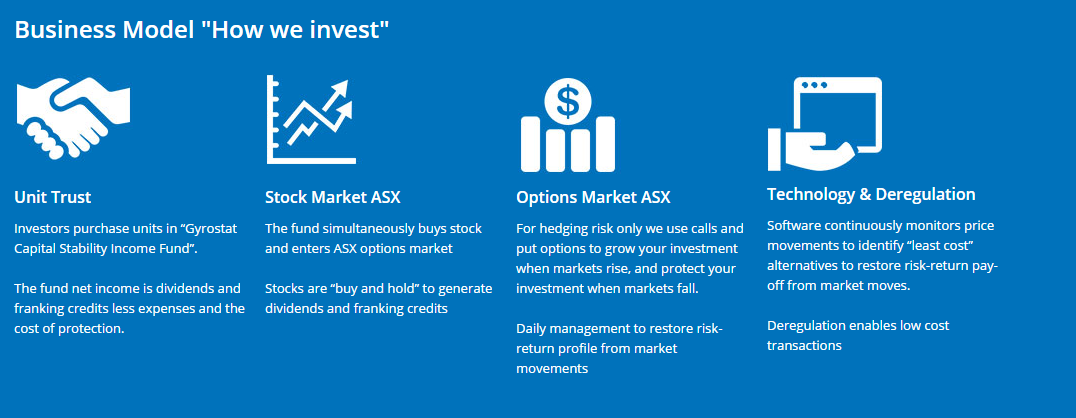

The perception has been historically that having protection always in place is ‘expensive’. Active management of the ASX options is the key to lowering its cost. This is enabled by developments in technology and deregulation.