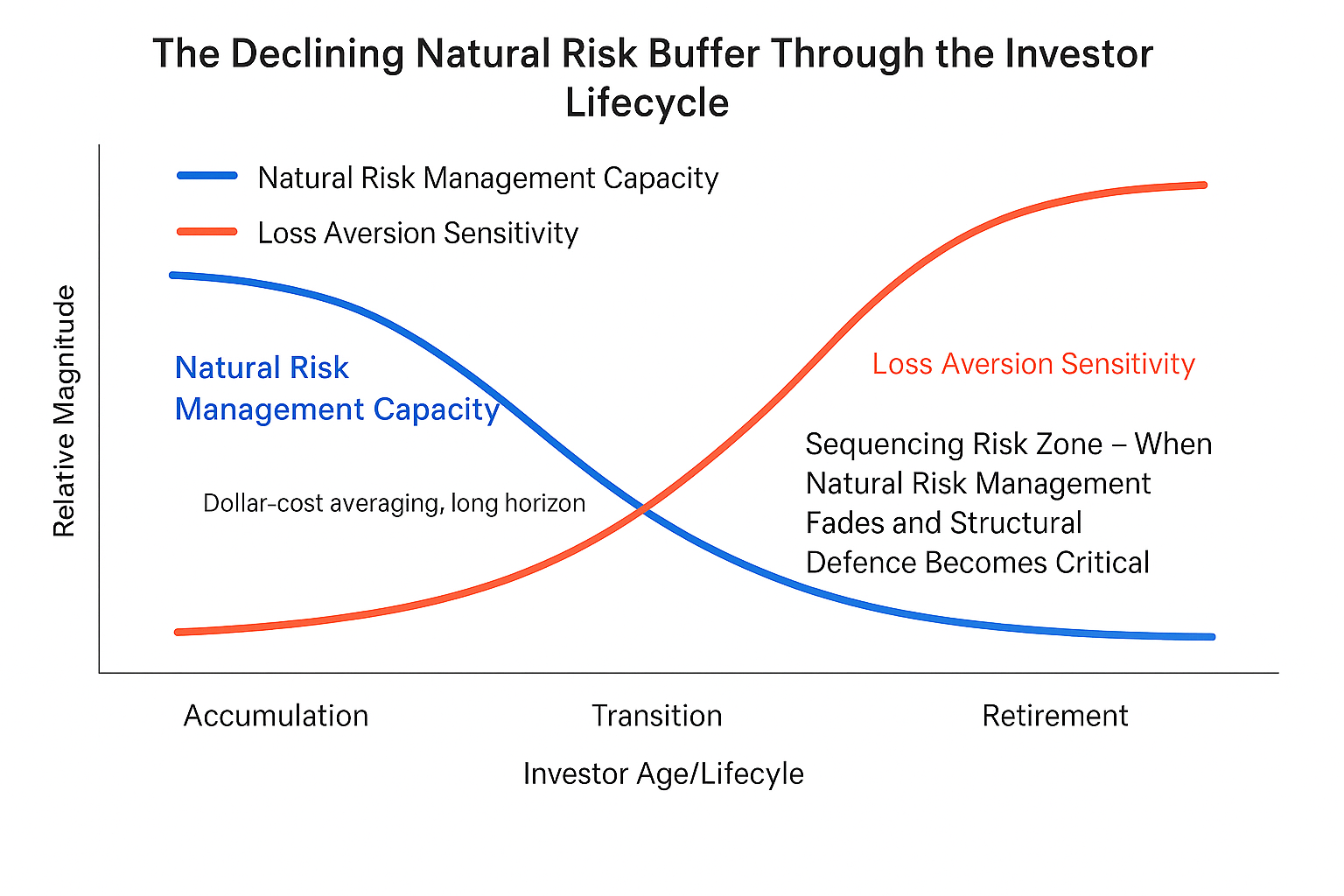

The Behavioural Crossover: Why risk management fades when we need it most

As investors transition to retirement, the financial and psychological equations invert:

• Contributions stop; withdrawals begin. There is no new capital to average down losses.

• The portfolio is now finite. Investors frame wealth not as future opportunity, but as lifetime security.

• Loss aversion peaks. A 10% decline in retirement feels catastrophic because it directly threatens lifestyle sustainability

This shift transforms volatility from friend to foe. The same 10% drawdown that was tolerable at 40 years old becomes intolerable at 65, not because of numbers, but because of context.

This is where sequencing risk emerges: losses early in retirement inflict damage that time and income cannot easily repair.

Advisers now face a paradox: encouraging patience no longer works because patience is no longer protective. The solution must therefore move from behavioural coaching to structural risk design.