In financial markets, uncertainty is a constant. But in retirement portfolios, uncertainty carries asymmetrical consequences. A portfolio can recover from volatility; a retiree cannot recover from a major drawdown early in retirement. This is the essence of sequencing risk, and it is the most overlooked threat facing investors today. Much of the current debate focuses on whether global equity markets are priced for perfection, or whether the extraordinary rally in AI-linked mega-caps has further to go.

But this focus on prediction distracts from the more fundamental question: What are the consequences if we’re wrong? This is the question advisers must answer, not because of forecasting skill, but because of stewardship responsibility.

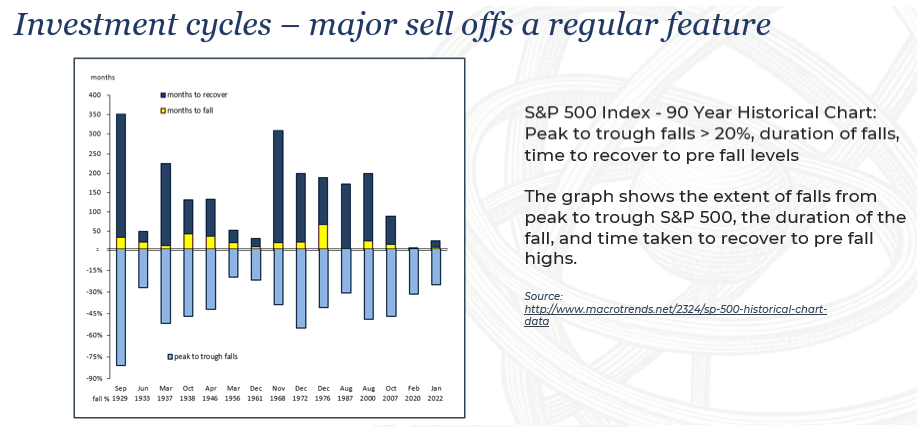

View the full article as published in Global Financial Market Review here.