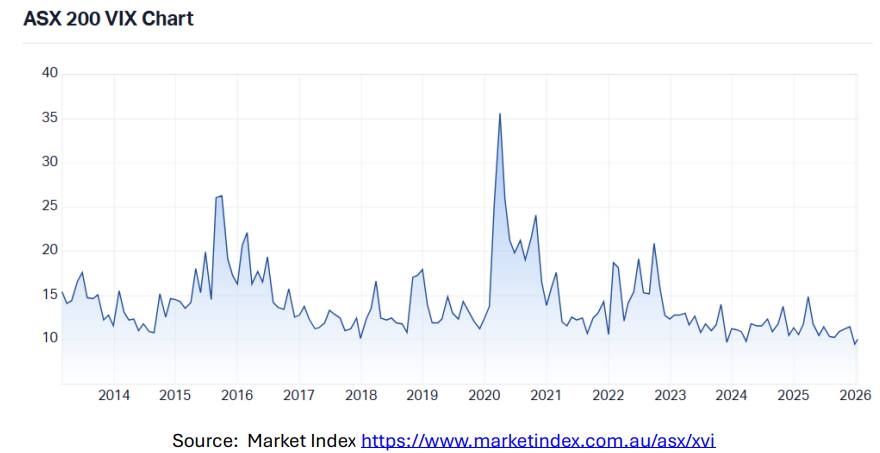

Pricing of risk: calm at multi-year extremes

Australian equity volatility is currently priced at levels rarely seen over the past decade. Measures of implied volatility, including the A-VIX, sit near multi-year lows, signalling a market environment that appears calm, stable and well-behaved. Periods like this are often interpreted as benign.

Yet from a risk-management perspective, they are better understood as moments when risk is being cheaply priced rather than absent. Low implied volatility reflects low demand for protection, not low exposure to uncertainty. Historically, such conditions have coincided with increased complacency, narrower risk premia and a growing reliance on stability assumptions — precisely the conditions that matter most for retirees and income-dependent investors.